AVFINPAL is your financial pal and buddy, where financial insights meet Simplicity. Delve into the realms of financial management and wealth creation as we unravel the complexities of money matters. Here, you will get expert insights and actionable strategies converge to guide you on a path to financial mastery. Join me on this journey as we explore investment opportunities, navigate market trends and craft bespoke financial decisions.

Budget 2019 - Taxation

Get link

Facebook

X

Pinterest

Email

Other Apps

Finance Minister Piyush Goyal presented the most awaited union budget in Lok Sabha on Friday, 1st February 2019. Goyal was appointed as the interim finance minister on January 23with Arun Jaitely undergoing medical treatment in United States. Here is a look at some of the major tax changes proposed in the budget.

Income Tax slabs will remain the same for FY 2019-20. Yes, there is no change in the slab rates for the financial year 2019-20. Tax Rebate Limit under 87A has been increased from Rs. 3.5 lakhs to Rs. 5 lakhs for taxpayers. The maximum limit of the tax rebate is also increased to Rs.12,500 from the present limit of Rs. 2,500. Hence The benefit of this rebate is available only to the middle and lower middle class assesses only and assesses having taxable income more than 5 Lakhsmay not have much of the benefit from this.

How will it be implemented?

Let us understand this with a simple example of

Mr. A has a total taxable income of Rs 5 Lakhs and Mr. B has an income of Rs.10 Lakhs.

Now first Let us see how their tax computation use to happen before the proposed changes Now let us see the computation after the proposed changes

No tax on notional rent of second Self-occupied House under “Income from House Property” i.e. up to two self-occupied house properties to be considered for exemption.

What Does This Mean?

If you have three house properties, out of which you live in one of them, and the other two are not given on rent, then any two out of three house properties can be considered as 'self-occupied'. The third one will then be considered as deemed to be let out and taxed accordingly.

Earlier, if an individual had more than one house, then apart from the self-occupied property, the second home was subject to income tax on notional rental income. This meant that even if the second house was lying vacant, an individual was required to pay tax on the notional rental income (calculated as per tax rules). Currently, this second property is treated as a deemed-to-be let out property and is treated like a rented property even if it not given on rent, as per current income tax laws. However, once the proposal made in the budget 2019 is passed by the Parliament, you will not be required to pay income tax on second house property. What about the interest on housing loan and carry forward Losses?

The deduction for interest on housing loan for the two self-occupied house properties shall not exceed Rs 2 lakh. Remember currently, on your second house property, you could carry forward the losses up to 8 assessment years in case the loss from house property exceeds Rs 2 lakh in a single fiscal year. After the proposal is passed, you will not be able to carry forward these losses from your second house property.

TDS limit under Section 194A hiked from Rs 10,000 to Rs 40,000 on Post Office Savings and Bank Deposits.

Standard Deduction for the salaried class increased from Rs 40,000 to Rs 50,000.

What is Standard Deduction?

It is a fixed amount of deduction which can be reduced by salaried taxpayers, from their gross salary. It was introduced by the Arun Jaitley in the budget of 2018 last year. Interestingly, the provision of Standard Deduction was earlier available but was abolished in the Finance Act 2005. It was proposed that this deduction would replace then existing transport allowance of Rs 1600 per month and medical allowance of Rs 15,000 per annum. They were usually deducted from the gross salary and claimed as an exemption. How does it affect you?

This Standard deduction will be playing a great role for in the taxation of those assesses who are having a total taxable income of more than Rs. 5 lakhs

Section 54 exemption now available on the second house property, provided the capital gains is less than or equal to Rs. 2 crores – to be availed only once in a lifetime.

How Is this Going to work?

Under section 54 of the I-T Act, to save on the capital gains made on the sale of a residential property, one is currently allowed to invest only in one house property. The Finance minister in the budget speech stated that the benefits roll over exemption of capital gains under section 54 of the Income Tax Act will be increased from investment in one residential house to two residential houses. Are there any conditions attached to it?

Well yes, of course, there are certain conditions attached to it :

To claim the exemption, a new residential house property must be purchased 1 year before the sale or 2 years after the sale of the property/asset or constructed within 3 years of the sale of the property/asset. The benefit is available only if the new residential properties are situated in India.

This benefit can be availed only once in a lifetime.

Keep on making such important blog post. Your work is really being appreciated by someone.A very nice informational blog tax return for self employed in London

Let’s face it—home loans are a huge financial commitment. They’re often the most significant debts many of us take on, stretching across decades. But here’s the good news: paying off that loan early could unlock so much financial freedom. It can reduce stress, save you tons in interest, and free up cash for other important things—whether that’s investments, savings, or enjoying life a little more. But before you jump into early repayment, it’s important to weigh the benefits. Sometimes, it may be better to invest your extra funds if the returns are higher than what you’re paying in interest. After all, home loans tend to have lower interest rates compared to personal loans or credit card debt. So, figuring out the right balance is key. If you’re leaning towards paying off your loan early, here are five practical strategies that could help you get there faster. 1. Lump-Sum Repayments: Using Windfalls Wisely Scenario: Priya has a home loan of ₹1 crore at 8% interest rate for...

Hi Folks, I had an interesting discussion with my fellow portfolio managers in my team last week. The discussion hovered around the greater changes that are being brought about in India's economy, which is expanding faster than most of its peers. With increasing spending as a result of rising salaries, more people are treating themselves to expensive luxury goods and antiques. It's overwhelming to how the Indian market is evolving and investors are looking into alternate asset classes and items like high-end watches, rare wines, whiskey, sneakers, and fine art are emerging in the Indian Economy too. This whole discussion led me to dig into some insights about how these alternate assets classes actually sailed over the years. Eventually, I thought be a good idea to share some of these insights with my readers. It's interesting to note that luxury timepieces are fast emerging as a new source of fixation for the wealthy, particularly Gen Z and millennials. Younger co...

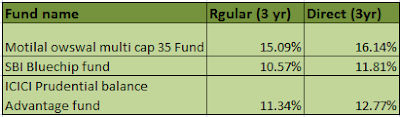

Almost Every mutual fund comes under two versions- Direct plans and regular plans. The main difference between the two is that regular plans have a distribution commission and direct plans don't. But is that the only difference? And does that really matter to an investor? well, yes it does matter. To elaborate this, let us see how direct plans are better than regular mutual fund plans. 1. Higher returns The returns of any direct mutual fund are always higher than the regular version of the same mutual fund. One of the key factors which influence a mutual fund investment decision is the return. The return of a mutual fund is usually calculated on 1 year, 3 years, and 5 years basis to represent the traditional investment horizon. The returns in case of direct mutual funds are always higher than their regular counterparts. Here are a few examples. ...

It is really quality & outstanding post. keep it up!

ReplyDeleteLatest stock market news and updates on the stockinvestor...buy or sell stock ideas by experts for minute to minute updates...

StockTrading

Stock Trading

Share Trading

Share Trading

Wonderful blog.. Thanks for sharing informative blog.. its very useful to me..

ReplyDeletetax return for self employed in London

Keep on making such important blog post. Your work is really being appreciated by someone.A very nice informational blog

ReplyDeletetax return for self employed in London

hi,its fabulous post.you doing good job

ReplyDeleteonline accounting services