Have you planned for your retirement?

How do you envisage your retired life? Relaxing at some exotic location, following all your dreams and passion which you once left behind to make a better living. On the flip side, it can be horrifying where you are dependent on your kids, living a life where you have to think twice even before spending on the basic necessities. Well, I am sure no one wants to works a major part of the existence just to survive for the rest of their lives. We all wish for a lavish and relaxed post-retirement life. But do we all even do something for it? Even if many of us do think of it. We lack the proper direction. Well, the best way to fulfill all your post-retirement goals is to start saving for it from today itself. In fact not just save you need to start Investing for it. Obviously, what's the fun of seeing your money resting in a savings account, while you are working your soul off. Its time you put your money at work too.

In this article, we will be comparing various investment avenues available for the investors, which can help them secure a comfortable investment corpus.

Retirement planning is divided into three phases’ investment, accumulation and withdrawal. Investing in mutual fund can easily facilitate all these phases. Successful achievement of these phases depends upon the various factors like risk and return profile during the investment phase, liquidity or access to the money during the accumulations phase and taxability during the withdrawal phase.

Risk And Return:

When it comes to investing the two basic things every investor looks for are the risk associated with the investments and the return the investment would be generating corresponding to that risk. However it is very important to carefully study the risk- return profile of the investment before investing. Where the investment options like NPS , PF and some post office scheme are backed by the strong nexus and support of government and are can be considered to be highly secured. The avenues like bank FD, insurance policies and mutual fund investments which are backed by the regulatory bodies like RBI,IRDA and SEBI respectively are comparatively more risky.

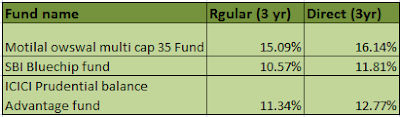

These risk factors is what differentiate the returns of these avenues. Though government backed option are safer but provide a low to moderate return of around 5-7 percent per annum ( approx) . Whereas a little riskier avenue like mutual fund can provide a much better return of around 12-15 percent year on year, if held for long term.

Liquidity and ease of access to money:

Once we have chosen the investment avenues and have started to accumulate our money in a high growth avenue. The next concern we face is how easily can I liquidate my money if we need it in case of emergency. Avenues like NPS and PPF though are safer comparatively but carry a long lock-in period. Like the amount invested in PPF is locked for 15 years, i.e. amount once invested in PPF can be redeemed before a period of 15 years. Same is the case with NPS which to comes with a lock-in period depending upon the age you are starting it.

Similarly, retirement benefit insurance policies comes with a lock-in period and even if there is no lock-in period they charge a heavy amount on surrendering or stopping the policy.

Whereas the amount invested in a mutual fund is highly liquid and can be redeem or taken out from the fund any time

Taxation.

Once we have successfully accumulated the required amount of corpus for a peaceful retirement the next thing we have to check is the amount of tax we will have to pay on the withdrawing from the corpus. Where, PPF offers you a tax free withdrawal from the corpus. The NPS allows you to withdraw 60 percent of the amount tax free but remaining 40 percent is charged at tax as per your effective slab rate.

Similarly, the amount invested in bank FDs and retirement policies are fully liable to tax at the time of withdrawal.

However, the amount invested in a mutual fund can be withdrawn in a very tax efficient manner and can provide the best post tax returns. The tax on mutual funds can be as low as zero to ten percent. That is why mutual funds are said to be the most tax efficient way to draw a pension from your corpus.

In this article, we will be comparing various investment avenues available for the investors, which can help them secure a comfortable investment corpus.

Retirement planning is divided into three phases’ investment, accumulation and withdrawal. Investing in mutual fund can easily facilitate all these phases. Successful achievement of these phases depends upon the various factors like risk and return profile during the investment phase, liquidity or access to the money during the accumulations phase and taxability during the withdrawal phase.

Risk And Return:

When it comes to investing the two basic things every investor looks for are the risk associated with the investments and the return the investment would be generating corresponding to that risk. However it is very important to carefully study the risk- return profile of the investment before investing. Where the investment options like NPS , PF and some post office scheme are backed by the strong nexus and support of government and are can be considered to be highly secured. The avenues like bank FD, insurance policies and mutual fund investments which are backed by the regulatory bodies like RBI,IRDA and SEBI respectively are comparatively more risky.

These risk factors is what differentiate the returns of these avenues. Though government backed option are safer but provide a low to moderate return of around 5-7 percent per annum ( approx) . Whereas a little riskier avenue like mutual fund can provide a much better return of around 12-15 percent year on year, if held for long term.

Liquidity and ease of access to money:

Once we have chosen the investment avenues and have started to accumulate our money in a high growth avenue. The next concern we face is how easily can I liquidate my money if we need it in case of emergency. Avenues like NPS and PPF though are safer comparatively but carry a long lock-in period. Like the amount invested in PPF is locked for 15 years, i.e. amount once invested in PPF can be redeemed before a period of 15 years. Same is the case with NPS which to comes with a lock-in period depending upon the age you are starting it.

Similarly, retirement benefit insurance policies comes with a lock-in period and even if there is no lock-in period they charge a heavy amount on surrendering or stopping the policy.

Whereas the amount invested in a mutual fund is highly liquid and can be redeem or taken out from the fund any time

Taxation.

Once we have successfully accumulated the required amount of corpus for a peaceful retirement the next thing we have to check is the amount of tax we will have to pay on the withdrawing from the corpus. Where, PPF offers you a tax free withdrawal from the corpus. The NPS allows you to withdraw 60 percent of the amount tax free but remaining 40 percent is charged at tax as per your effective slab rate.

Similarly, the amount invested in bank FDs and retirement policies are fully liable to tax at the time of withdrawal.

However, the amount invested in a mutual fund can be withdrawn in a very tax efficient manner and can provide the best post tax returns. The tax on mutual funds can be as low as zero to ten percent. That is why mutual funds are said to be the most tax efficient way to draw a pension from your corpus.

Comments

Post a Comment