Personal Finance Tips for Young Professionals Starting Their Career

Being a millennial has its virtues and shortcomings, but more often than not, millennials are considered to be financially indisciplined, frittering away their money on avocado toasts and lattes.

Recently, one of my clients brought his son to me for a session on personal finances and investments. The main concern of the father-son duo was that they weren't able to figure out where all the salary is going and how can he be more prudent towards his finances.

While having a discussion with him I realized that the issues he has been facing are common among the young professional and the main problem was lack of financial literacy and the segregation and consensus of the young generation's mindset from their parents.

So in this article, we will be discussing the aspects of finances that every young professional should consider to manage their finances in a more responsible manner (as their father would want them to).

1. Pay Yourself First: Before you get on to pay the vendors for the groceries or the restaurant owner for the rocking party you planned for the weekend or to the online store for that fancy gadget you had eyes on for long now and even before you pay homage to the family, pay yourself first.

Every time you get your salary or any other income the first thing you have to do is to put a certain percentage of that income aside for your savings and investments. You have worked hard for that money the first right on that money is yours, always pay yourself first.

For starting you should aim to save about 10- 25% of your monthly income and the remaining 90-75% should be utilized for your needs and wants. This percentage shall depend on your income and your status. if you are staying in PG or on rent away from home you can aim for saving at least 10% and if you are comfortably habituated with your family you easily save up to 25% and can gradually adjust this percentage as per your comfort.

Caution: Don't go below 10% for more than 3 months also don't go overboard with saving too much that you start compromising too much. As in both these cases, the saving habit won't be much sustainable and you will eventually stop it.

2. Put your money at work: So by now, we have understood that priority has to be given to the savings before we start expanding. The next thing to be done is to put that saved money to work for you.

If you save the money but don't invest well over the period of time it will eventually become dead money. You have been disciplined have been able to save a good percentage on monthly basis but the money is lying in your piggy bank or in saving bank account is not actually growing instead it is reducing.

The simple concepts are understood here are Asset and Inflation. An asset is something that gives you something in return, so as per this definition money at the piggy bank which is not getting you any return is not an asset but you can conclude the fact the savings bank earns you an annual return on the money and hence it is an asset? Well not really ...

Allow me to introduce inflation. Inflation is nothing but the general rise in the prices of commodities and services in the country. Currently, the Inflation rate in India is around 5%. That means if an apple cost Rs.100 today one year later it would cost you around Rs.105. However, the return that savings banks are offering is around 2.5% to 4% annually. What this means is that your savings are increasing by 2.5% in one year whereas your expenses are growing by 5%. So if you observe your money has not grown by 2.5% instead it has degraded by 2.5%.

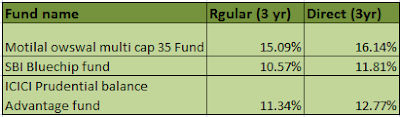

So, what's the way out, you ask? Well, the simple and obvious answer is to start investing your money in high growth rate products which can give you inflation-beating results. The easiest and most viable options for the layman to invest are mutual funds, bank and corporate FDs.

For more information on where to invest, I highly recommend going throw my previous blogs on this topic.

3. Cut Down Your Expenses: It's time we talk about the elephant in the room and discuss the topic that we all are lectured the most from our parents. Yes, I am talking about spending mindlessly or as I call it spending unconsciously.

It so happens that we fail to understand that the tiny amount spends on eating out or on the food delivery apps might not pinch at that moment. But those weekend party that seemed to be just Rs.1,000 at that particular day amounts to 5,000 per month for the 5-weekend party you had. You need to start seeing your money with a holistic view rather than seeing them in isolation.

The best way to cut off your extra expenses is to have a predetermined budget but keeping a budget is again so uncool. Well yes I do agree keep and maintaining a budget for every single thing might come hand to our generation but here comes the thing we are good at - technology. Yes, the millennials have been blessed with the technology and their various apps you can use to keep a budget and if you are lazy for even that handiest way will be to just keep checking your account balance every week and notice your transaction inflows and outflows.

Next time you spend 5000 in a month on just-food try to calculate what those Rs. 5,000 could have gained you in the next 2 years had you invested that amount on monthly basis rather than pleasing your taste buds.

4. The New Mindset: The studies have shown that the new generation is less inclined towards the traditional mindset of owning a house and even purchasing a car.

A decent house in a metro city would cost you approx 70-90 lakhs and if you plan to finance it through a bank you would have to pay an interest of approximately 7% annually. Suppose you took a loan of Rs. 75 lakhs for 15 years from a bak at 7 % interest that bank would charge you.

You will be ending up paying a monthly amount of Rs. 67,400 and by the end of the 15th year you would have paid an amount of Rs. 1.21 Crore. Which means you are paying an interest of Rs. 51 lakh approx. Means actually the house has cost you 1.21 crore but its value probably much less than that.

On the flip side to decide to go for rented accommodation in a well-developed locality or maybe going for modern housing solutions like Airbnb and Nest-away houses. The monthly rental would be around Rs. 30,000 which is almost half of the EMI you would be paying on your home loan and would also save you the cost of maintaining and restructuring it.

And even worse is the scenario in the case of a car. Purchasing a basic small car would cost you around 4 - 4.5 lakhs and if you finance it you will be charged an interest of around 8% annually until you repay the loan. But god bless the technology we have cab rides available on our phones. A general cab ride from home to office and back would cost around Rs. 400 and considering you have 265 working days in a year, you can conveniently complete your annual travel cost in just Rs. 1.06 lakhs that would be approx one-third of the cost of owning a car.

So Shouldn't we aim for owning a house or a car? Does that mean we should overlook our ambitions in life?

Well, I have nowhere intended to say that you shouldn't aim for a car or a house the Idea is not to rush for these luxuries at the initial stage of your career. At the initial stage aim for setting up a financial base for your self and later in life you can aim to utilize your finances and your invested amount to go for a house or a car.

In the case of a car or a bike or a gadget, one simple rule that is to be remembered is that don't buy something you can't afford to buy it for the second time.

The common mistake we all do is to overjudge our buying capacity. The credit cards and no-cost EMI's comes with an equal amount of disadvantages as much as they have the advantages. Buying the latest iPhone worth 1 lakhs when your CTC is 4 lakhs isn't a wise move.

Note: Views expressed above are solely the author's perspectives. Readers are advised to keep their discretion insight before making any investment.

Also read:

Explained so wisely. I will surely abide by your words.

ReplyDelete