Basic Frame work - Income Tax

Paying income tax and filing your return can be a confusing task especially if you lack the basic knowledge of income tax. If you are someone who has been just out of college or someone who will be filing his or her return for the first time the nitty-gritty of income tax may bother you but we have got your back. Your finpal aims to simplify investment and taxation for you and make your financial lives easier. In this taxation series, we previously shared the importance of filing the return. Continuing that here is the basic structure of income tax.

The financial year or previous year refers to the year in which the income which is subject to tax has been earned or accrued. This is usually a 12 month period starting from 1st April and ending on 31st March. No matter which month you start your job your financial year ends on 31st March.

Assessment year: It is the most common term you will come across while filing your return. It refers to the year subsequent to the year in which your income has been earned. That is the year following the Financial year is known as your assessment year. It is called assessment year because the income you have earned and proof of income you have filed are put to assessment in this year and return is to be filled in this period.

Let's understand it with the help for an example: Suppose you are a salaried person. The salary you have earned from 1st April 2018 to 31st March 2019 ( i.e. your financial is year 18- 19) will be taxed and assessed in the period of 1st April 2019 to 31st March 20 ( i.e. your assessment year is 19-20).

You will have to file your return of income up to 31st July 2019.

Any rental income from the house property (which includes any commercial property or any other type of property) is taxed under this head. However, if the property hasn't been let out the tax is charged on the basis of expected rent that would have been received if the property had rented out.

Thus you are charged for both the property which is let out on an actual basis as well as on the property which is not let out on a notional basis.

Various deduction like the standard deduction, municipal tax paid and interest on home loans are allowed under this head.

TDS on rent @ 10% is also deducted in case the value of rent is more than the specified limit.

Note: The union budget 2019 has proposed an extra benefit under this.

Read: Budget 2019- Taxation.

Profit or gains arising from the transfer of capital asset made during the financial year shall be chargeable to tax under this head and shall be deemed to be this income of the year in which transfer took place. However, there are some exemption under section 54, 54B, 54D, 54EC, 54F, 54G that are provided under this head.

Any stream of income which is not chargeable to tax under any other head of income is chargeable to tax under this head provided income isn't exempt from tax.

Deductions allowed from the total income are one of the best tools for your personal finance as they help you reduce your tax burden and allow you investment or savings in some cases.

The most common and highly recommended of such deduction is Section 80C of the income tax act.

1. Taxation year.

The financial year or previous year refers to the year in which the income which is subject to tax has been earned or accrued. This is usually a 12 month period starting from 1st April and ending on 31st March. No matter which month you start your job your financial year ends on 31st March.

Assessment year: It is the most common term you will come across while filing your return. It refers to the year subsequent to the year in which your income has been earned. That is the year following the Financial year is known as your assessment year. It is called assessment year because the income you have earned and proof of income you have filed are put to assessment in this year and return is to be filled in this period.

Let's understand it with the help for an example: Suppose you are a salaried person. The salary you have earned from 1st April 2018 to 31st March 2019 ( i.e. your financial is year 18- 19) will be taxed and assessed in the period of 1st April 2019 to 31st March 20 ( i.e. your assessment year is 19-20).

You will have to file your return of income up to 31st July 2019.

2. Heads of income.

Whatever income you earned during a year, by whatever means or by whatever source are categorized into 5 different groups. These groups are known as heads of income. The total income under all these 5 heads is then added up and is disclosed in your income tax return. Let us have a short summary of these heads.a. Income From Salary.

Any income can be taxed under the head of the salary only if there is a relationship of an employer and an employee between the payer and the payee. If this relation doesn't exist, income can't be deemed to be the salary income.

b. Income From House Property.

Any rental income from the house property (which includes any commercial property or any other type of property) is taxed under this head. However, if the property hasn't been let out the tax is charged on the basis of expected rent that would have been received if the property had rented out.Thus you are charged for both the property which is let out on an actual basis as well as on the property which is not let out on a notional basis.

Various deduction like the standard deduction, municipal tax paid and interest on home loans are allowed under this head.

TDS on rent @ 10% is also deducted in case the value of rent is more than the specified limit.

Note: The union budget 2019 has proposed an extra benefit under this.

Read: Budget 2019- Taxation.

c. Income From Profit and gains from a business or profession.

All the incomes earned by way of any business, profession, manufacture, commerce, trade etc are taxed under this head after allowing specific expenses as deductions.

d. Income From Capital Gain.

Profit or gains arising from the transfer of capital asset made during the financial year shall be chargeable to tax under this head and shall be deemed to be this income of the year in which transfer took place. However, there are some exemption under section 54, 54B, 54D, 54EC, 54F, 54G that are provided under this head.

e. Income From Other Sources.

Any stream of income which is not chargeable to tax under any other head of income is chargeable to tax under this head provided income isn't exempt from tax.3. Deductions.

Deductions reduce your Gross Income. These are the amounts Income tax department allows you to reduce your Income, bringing down your tax liability. These deductions are majorly confined under section 80C to section 80U. Tax is calculated on the net income after allowing all the deductions.Deductions allowed from the total income are one of the best tools for your personal finance as they help you reduce your tax burden and allow you investment or savings in some cases.

The most common and highly recommended of such deduction is Section 80C of the income tax act.

As per this section, if an individual or Hindu Undivided Families (HUFs) invests in or spends on specified avenues then up to Rs 1.5 lakh, as per the current laws, of this investment/expenditure can be claimed as a deduction from gross total income before calculating tax payable on it in a financial year. The deduction can be claimed only from income in the financial year in which the specified investment/expenses are made.

Given below is the list of some commonly used investments that are covered under this section and can be used as great tools for wealth creation or retirement planning:

a. Public Provident Fund

b. Tax Saving Fixed Deposits

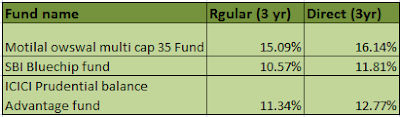

c. Tax Saving Mutual Funds.

4. Tax deducted at source or TDS

This refers to the process and amount deducted by the person making the payment. The person making the payment has to deduct tax as per the prescribed rules. If the TDS has to be deducted on your income by the person making payment to you for that income in that case you don't have to pay tax on that income again. That means you are saved from making a payment of tax from your own pocket, although ultimately it has been deducted from your income only. The person deducting TDS has to make the payment for tax deducted by him to the government.

5. Calculating Tax payable

Final Tax payable = Tax on total income - Tax deducted at source.

Very helpful! Thanks Abhinav :)

ReplyDelete